The Credit Crunch, Close Up and PersonalBy Olivier Garret – CEOCasey Research, The Casey ReportWithin the last year, the true extent of the real estate debacle and ensuing credit crisis in the United States has become blatantly obvious.

But now there is a new phenomenon rearing its ugly head: a credit crisis of the individual that is hitting a large number of Americans straight in the pocketbook. The reason: credit providers have started to batten down the hatches.

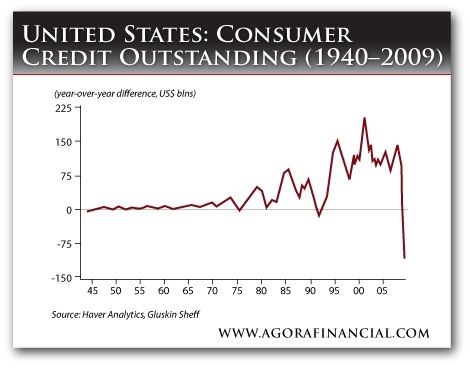

According to a November report by the Federal Reserve, nearly 60% of banks severely tightened their lending standards on credit card loans and 65% on other consumer loans in the last three months. As unemployment and delinquency rates go up and lenders are trying to minimize their risk, the average American all of a sudden finds himself cash strapped… this at a time when home equity has dried up, 401(k)s and IRAs are losing value by the day, and many common stocks are barely worth the paper they’re printed on.

“We’ve been hearing about the liquidity crisis affecting banks for quite a while,” Joe Ridout, spokesman for the advocacy group Consumer Action, told the Washington Post. “Now we’re seeing it transform into a crisis affecting people’s personal finances as well. The next wave of the financial crisis may well be a credit-card-related crisis.”

Credit card companies are indeed clamping down hard on customers. Many Americans may have noticed that while their mailbox used to burst with junk mail of the “You’re Pre-Approved!” sort, these days the influx has slowed down to a dribble. That’s no coincidence – credit card direct mail offers in the third quarter of 2008 have seen a 28% drop year-over year as Visa, AmEx & Co. are struggling to cope with a tidal wave of defaults.

Moody’s Investors Service reported that charge-off rates rose 48% in August compared to the same month last year, the 20th consecutive year-over-year increase. This number is expected to go even higher in 2009, potentially exceeding the charge-off rates during past recessions.

Thus, credit card members are increasingly coming under scrutiny – and not just those in the subprime category. Customers with a credit score of 700, who were deemed “most creditworthy” just a year ago are not anymore. According to cardratings.com, 730 is the new 700.

The palette of “risk factors” has also broadened. Aside from late bill and mortgage payments, now location, profession, and even shopping behavior are considered. If you live in a high-foreclosure area, work in the real estate, auto, or construction business, and buy your household necessities at Wal-Mart, you’re likely on the target list.

One of the measures credit card issuers have devised to reduce risk is slashing credit limits in half. 60% of banks lowered the credit ceiling for existing nonprime and 20% for prime customers. And, as a testament that the intended “trickle-down effect” of the Fed’s massive rate cuts didn’t work at all, many companies have kept their interest rates at the same level or even raised them by two or three percentage points. Late fees, too, have been increased.

This tightening of credit translates directly to people’s shopping habits. While Black Friday weekend brought an overall growth of 0.9% in sales from last year, retail sales data show that that wasn’t enough to save the month of November. The MasterCard SpendingPulse reading noted that electronics and appliance sales dropped by 25% in November, luxury goods by 24%, and sales at clothing and department stores by 20%. Foot traffic decreased by 19% from 2007, meaning shoppers visited fewer stores.

C. Britt Beemer, CEO and founder of America’s Research Group, who has correctly predicted percentage changes in Christmas retail sales for 16 of the last 17 years, published his first negative forecast (of -1%) in 23 years, calling the 2008 Christmas shopping season a “perfect storm” for retailers.

Even as the average American is battening down the hatches and reining in consumption, the Federal Reserve seems to be going the opposite way, judging from the $700 billion bailout package that has – literally within weeks – ballooned into an estimated $8.5 trillion colossus. But despite throwing fistfuls of money at the problem, says Bud Conrad, Casey Research chief economist and editor of

The Casey Report, “all the king’s horses and all the king’s men haven’t been able to put Humpty back together again.”

We don’t know whether the Humpty Dumpty economy can be saved… what we do know, though, is that every crisis holds danger and opportunity. By making the trend your friend instead of swimming against the stream, you can preserve your assets and profit handsomely, especially in highly volatile environments like the one we are seeing now. To learn more about how to generate double- and triple-digit returns in a crisis,

click here.

{kind=link}