So which will it be...IN-flation, or DE-flation? That's the $52 trillion question at this point. There are many worthy opinions to consider on each side of the debate. But who's right, and who's wrong?

I think it's important for us individual investors/traders to keep an open mind to all thoughtful, intelligent argumets. Which leads me to the stellar guest piece of inflation/deflation analysis that I'm excited to share with you today.

Jon really outdid himself in his Q3 update for 2009 - when he was kind enough to forward me a preview copy of his newsletter, I said: "Jon - this rocks! Can we please post this on the blog?"

So without further adieu, here a very objective, insightful look into the inflation/deflation situation. While Jon currently sits on the other side of the fence from me here (and we definitely hassle each other about this!) - this is a must-read for all serious investors, no matter which side of the inflation/deflation debate you believe right now.

It will definitely challenge your thinking and provide you with some new ways to look at this debate, especially how lagging productivity may turn out to be a dark horse deciding factor.

(And PS - make sure to visit Jon's site for more sharp investment analysis like this: https://www.ledererpwm.com).

***

Unproductive Inflation Down the Road?

The outlook for inflation has far reaching implications on many aspects of financial decision making. In the investment-management arena, inflationary expectations help shape asset-allocation strategies because certain asset classes (e.g., precious metals) perform better in high inflation environments while others (e.g., long-term government bonds) usually outperform when prices are stable or declining. Correctly determining which asset classes to over- and underweight is vital to generating competitive perfor- mance over time.

Following this recent historically severe financial crisis, the chasm between inflationary expectations is very deep. On one hand, many reputable economists have made compelling cases that low inflation or even deflation will persist well into the next decade. At the same time, others, including me, are concerned about higher inflation starting next year.

And if one believes Federal Reserve policy makers and the markets (see Figure 1), inflation will remain within a moderate 1-2% range for many years to come. (And why shouldn’t we believe the Fed after its interest-rate policies earlier this decade helped facilitate one of the worst financial crises during the past 100 years?)

Please click to enlarge.

While I would concur that slack labor markets, excess production capacity, and consumer deleveraging will lead to a low inflationary environment during the next 3-6 months, I still believe that the bigger risk is higher inflation down the road. As the economy begins to stage a recovery (albeit a moderate one), the combination of accommodative monetary policy and delayed government stimulus is likely to add fuel to the inflationary fire.

Perhaps more importantly, I would argue that lower private investment this decade will continue to hamper productivity levels, making it more difficult to achieve healthy economic growth and low inflation concurrently. When one also considers rising government budget deficits and an escalating U.S. national debt, the case that inflation will be higher than what the markets are currently pricing in becomes even stronger.

The Case for Low Inflation

If one observes Figure 1 (above) showing the 5-, 10- and 20-year TIPS spreads, which measure the difference between yields on Treasury Inflation Protected Securities (TIPS) and yields on Treasuries of equivalent maturities, one can see that the markets are currently pricing in modest inflation for some time.

Meanwhile, many economists have made persuasive cases for low inflation or even deflation well into the next decade. Their arguments are predicated primarily on the combination of slack labor markets, excess production capacity, and the overhang from an over-indebted consumer. Moreover, they note a recent breakdown in the relationship between money supply and inflation, citing the past 25 years when prices increased at a much lower rate than the money supply.

Slack Labor Markets

Recent history has shown that there is a relatively strong inverse relationship between unemploy- ment levels and wage growth and that wage growth and inflation rates are highly correlated (see Figure 2).

Due to the current recession’s severity, unemployment has spiked from 4.9% in January 2008 to 9.5% (June 2009). Considering the greater labor supply from more people being out of work, workers are now less able to command higher wages from employers. And with substantially lower labor union membership and more globalized labor markets relative to the 1970s (when wages actually increased with unemployment levels), it is difficult to envision higher wage pressures during the next 12 months even if the economy begins to recover. The absence of substantial wage growth would eliminate a key inflationary factor.

Excess Capacity

As a result of last year’s credit crunch, worldwide demand fell drastically, causing inventories to rise and manufacturers to scale back production. With industrial production virtually falling of a cliff, capacity utilization has dropped precipitously in most developed economies, including the United States. As Figure 3 shows, factories and other manufacturing facilities are operating well below their potential, thus reducing the likelihood that they will raise their producer prices in the near future.

Debt Overhang

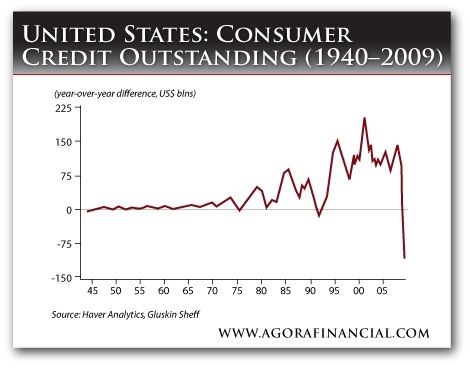

Despite the U.S. consumer in- creasing his savings rate from literally nothing in parts of 2005 and 2006 to nearly 7% in June 2009, total consumer debt to disposable income ratios remain elevated.

Given higher unemployment, coupled with a depressed housing market and a banking sector still reluctant to extend credit, there is a strong likelihood that consumers will continue to deleverage by saving money and reducing their debts. In doing so, they would be consuming less, thereby impairing economic growth and price levels.

One need look no further than Japan during the last two decades to observe the long-term defla tionary effects of a debt overhang. Such an example provides a strong case against higher inflation during the years ahead.

Money Supply and Inflation

In theory, if the money supply increases, higher inflation should result because there is more money pursuing the same amount of goods and services. Empirically, the U.S. inflation rate generally tracked growth in the money supply from 1960 through the early 1990s. However, since that time, the relationship has deteriorated somewhat (as shown in Figure 5).

Those in the low inflation / deflation camp point to this breakdown and argue that the sizable increase in money supply during the past year (9% growth in the M2 money supply from June 2008 to June 2009) will not necessarily drive price levels materially higher.

The Case for Higher Inflation

Despite the deflationary forces mentioned in the previous section, I continue to believe that longer-term inflation will exceed what the market is currently forecasting. Once the economy begins to recover (the capital markets appear to be pricing in a recovery later this year), I think the combination of the Federal Reserve’s extremely accommodative monetary policy and delayed federal government stimulus will add upward pressure on prices.

I also think that subpar productivity growth resulting from declining private investment this decade will make it more difficult to achieve healthy economic growth at lower inflation levels. Moreover, considering the large U.S. government budget deficits and the inability of lawmakers to exercise fiscal restraint in the face of looming entitlement expenditures (e.g., Medicare and Social Security), I remain concerned that the U.S. government may keep resorting to the printing presses well into the next decade.

Loose Monetary Policy

On the heels of one of the worst recessions and credit crises since the Great Depression, I have found it surprising that inflation rates have not fallen more since last fall. As noted previously, core consumer prices, which exclude volatile food and energy prices, have still risen nearly 2% during the past 12 months in the face of higher unemployment, lower capacity utilization, and consumer deleveraging. I would argue that one of the primary reasons price levels have continued to increase has been the Fed’s extremely accommodative monetary policy.

Since last fall, the Fed has thrown massive amounts of money into the financial system via both traditional means (e.g., lowering the Fed-Funds target rate) and unprecedented methods (e.g., providing subsidized financing to facilitate toxic-asset purchases) to try and stave off a deflationary spiral. While these maneuvers appear to have effectively warded off the Great Depression Part II, I am concerned that the Fed will have a difficult time unwinding these moves once an economic recovery starts to materialize.

Though the Fed’s new ability to pay interest on bank reserves will certainly help (because banks will have less incentive to lend out money if the Fed pays attractive rates on reserves), I do not think it is realistic to expect Fed policy makers to time their policies effectively. Considering that the Fed’s lax monetary policies played a significant role in the stock-market bubble during the late 1990s and the housing and credit market bubbles this decade, it should be evident that Fed policy makers have often been mistake-prone with respect to taking proactive steps to slow excessive growth.

In addition, with high unemployment levels and a President and Congressional leaders focused on adding jobs, the Fed will almost certainly be under immense political pressure to not take measures that would slow economic growth and proactively fight inflation.

Delayed Stimulus

On February 13, Congress passed a $787-billion stimulus package in attempt to spur an economic recovery. According to the Congressional Budget Office, nearly $185 billion of the stimulus is scheduled to be spent in 2009, with another $400 billion in 2010 and an additional $134 billion in 2011. Most of the remaining funds (roughly $70 billion) have been allocated to the years 2012-2014. Incredibly, of the stimulus money already available, only 35% has been paid out. (The government behind schedule due to inefficiencies – who could have predicted?)

Should the economy start to recover later this year, I fear that the massive amounts of stimulus money entering the system will drive inflation higher in 2010. Based on the most-recent U.S. economic figures, the $400 billion of stimulus in 2010 would addnearly 3% to gross domestic product (GDP) levels, excluding any multiplier effects.

Lower Productivity

Going into the next decade, I am concerned that lower productivity growth in the United States due to years of underinvestment will make it more difficult to achieve healthy economic growth without higher inflation.

When analyzing U.S. GDP data this decade, one can observe how the debt-fueled excess consumption since 2000 has resulted in less financial resources being allocated toward private investment, a key to long-term prosperity. Private investment impacts productivity growth, which enables producers to supply more goods and services at a lower cost. For this reason, countries that are more productive have higher standards of living.

I would argue that the United States during the post-war period provides several excellent contrasting examples of how productivity can impact inflation.From 1966-1982, private investment in the United States grew at a relatively tepid pace, falling below consumption growth and barely outpacing growth in government spending. As Figure 7 (below) shows, productivity growth averaged less than 3% (compound average growth rate, or CAGR) during this period.

Please click to enlarge.

Perhaps not coincidentally, core inflation hit elevated levels during the 1970s and early 1980s. While oil-supply shocks and flawed government policies certainly had a detrimental impact on inflation, I believe that the meager productivity growth also played a pivotal role.

From 1983-2000, private investment grew at a very healthy 6% rate, outpacing consumption and government spending growth by a wide margin. Not surprisingly, productivity increased at a 4.1% CAGR, while real GDP grew at a healthy 3.6% average pace. Even with substantially higher economic growth, the average inflation rate fell by nearly half (when compared to the 1966-1982 period), proving, in my opinion, that productivity growth is a vital ingredient to ensuring healthy economic growth without high inflation.

Since 2000, however, when debt-fueled excess consumption has shifted resources away from private investment (as consumers chose to spend instead of investing their capital in wealth-creating projects), private investment levels have literally declined. As a result, the rates of both productivity and GDP growth have fallen this dec- ade. While inflation rates have also been lower, I fear this trend may change relatively soon.

The Impact of Deficits

With the U.S. federal deficit recently reaching $1 trillion, the ratio of federal debt to GDP is expected to rise from 41% (in September 2008) to 55% by this September, according to the Congressional Budget Office. I fear such structural deficits and the rising national debt will amplify inflationary forces into the next decade for several reasons.

First, government budget deficits can crowd out private investment over time because higher interest rates (which result from lenders demanding greater compensation for the increased credit risk due to the escalating national debt) drive up the cost of investment capital.

While higher interest rates can slow the pace of economic growth and put the brakes on inflation, the longer-term impacts on investment and productivity growth can prove detrimental.

And though interest rates have fallen during the past 25 years while the national debt has risen, I believe this trend could change considering that rates are already near historically low levels.

Second, as debt levels rise, governments have an incentive to print more money and inflate their way out of debt (see Germany post-World War I and Zimbabwe today for extreme examples).

Considering the U.S. structural budget deficits and the inability of lawmakers to exercise fiscal restraint even in the face of looming entitlement expenditures, I am concerned that the printing presses will be very busy during the coming years, thereby increasing the money supply and inflationary forces. (We will see if the relationship between money supply and inflation will remain weak if productivity growth keeps declining).

Asset Allocation Strategies

Given my view that inflation rates will exceed what the markets are currently pricing in (using the TIPS spread as a proxy), I would recommend overweighting asset classes that should provide an effective hedge against inflation.

These asset classes include commodities (particularly precious metals), real estate, and TIPS. At the same time, in light of the very plausible case for low inflation or even deflation, it is important to maintain a diversified portfolio that includes exposure to long-term Treasury bonds and cash, which somewhat counterintuitively can provide a slight hedge against inflation (assuming the Fed were to raise short-term interest rates to try and maintain price stability).

Conclusion

It is difficult to remember a time in recent history when the gulf between inflationary expectations has been so wide. With all the uncertainty behind today’s inflation debate, I find it fascinating that the markets appear to be pricing in a long-range scenario where the Fed masterfully orchestrates monetary policy (to maintain core inflation within the Fed’s preferred 1-2% range). Considering the Fed’s track record of fueling bubbles during times of much less economic uncertainty, I would argue that it is a leap of faith to think that policy makers will get it right this time. Unfortunately, because of irresponsible fiscal and monetary policies this decade that came at the expense of investment-led productivity, I think we could literally be paying the price for years to come.

Thanks again to Jonathan Lederer for his sharing his excellent inflation/deflation analysis with us. And please be sure to check out his website, which contains more outstanding content! -Brett

{kind=link}

{kind=link}